Oracle's Q2 Results: The Real Story

Oracle's 2nd quarter results released last night has not de-railed the AI thematic, as suggested by headlines across financial media outlets. Still clocking in massive revenue growth (Oracle Cloud Infrastructure up 52%, GPU consumption up 336%), and more importantly, new customer growth — delivering diversification benefits to a supposedly "risky", highly-concentrated customer base after signing on OpenAI. The ink on that deal barely dry, and they've already added Meta.

The issue with the headlines is neither Oracle's debt-fuelled capex expenditure on data centres, nor the trajectory of AI adoption.

It is investors. And how irrational their perspectives can become, when the market's animal spirits are unleashed. Oracle was not the one pushing its share price higher, investors were.

Now, to be fair — the leverage concerns aren't baseless. But here's what matters more:

Here are two points to consider, following the Oracle results:

- Still in the infancy stage of AI adoption

The AI-related earnings growth will come, it is just a matter of timing. If we borrow the analogy of the S-curve, as exhibited historically during new technological adoptions, we are still sitting in the initiation phase. We could be on the tail-end of the initiation phase, or at the very start. Regardless. The growth phase has yet to come.

- Limited computing capacity, against surging demand.

Everyone knows AI has necessary equipment such as Nvidia's GPUs. Well, the chips themselves are manufactured at TSMC's fab facilities, which has something like a 6 month manufacturing duration, for just the wafering process.

And. As much as you try to, you cannot speed up the process — cutting corners will risk higher defect rates. Not good. But here's the bottleneck most people miss: TSMC's advanced packaging capacity (called CoWoS) is what integrates those GPUs with High Bandwidth Memory. That packaging process is severely constrained, with lead times stretching out months. The same capacity constraints apply to HBM production at SK Hynix and Samsung, which supply the memory modules essential for AI workloads. Try running an AI model locally, you'll see what I mean.

Point is, production capacity is limited.

Therefore, coming back to Oracle.

If the world can only produce a finite number of AI-capable GPUs a year, Oracle is solidifying its market share in the future right now, by buying as much as they can possibly get. Because, the number of GPUs you own represents the market share you will have in the future.

In fact, if a company operating in the data centre service space right now is not acquiring as many GPUs as they realistically could — well... your earnings from say... Year 3 or 4 onwards might evaporate as your equipment/assets lose relevance in an AI world.

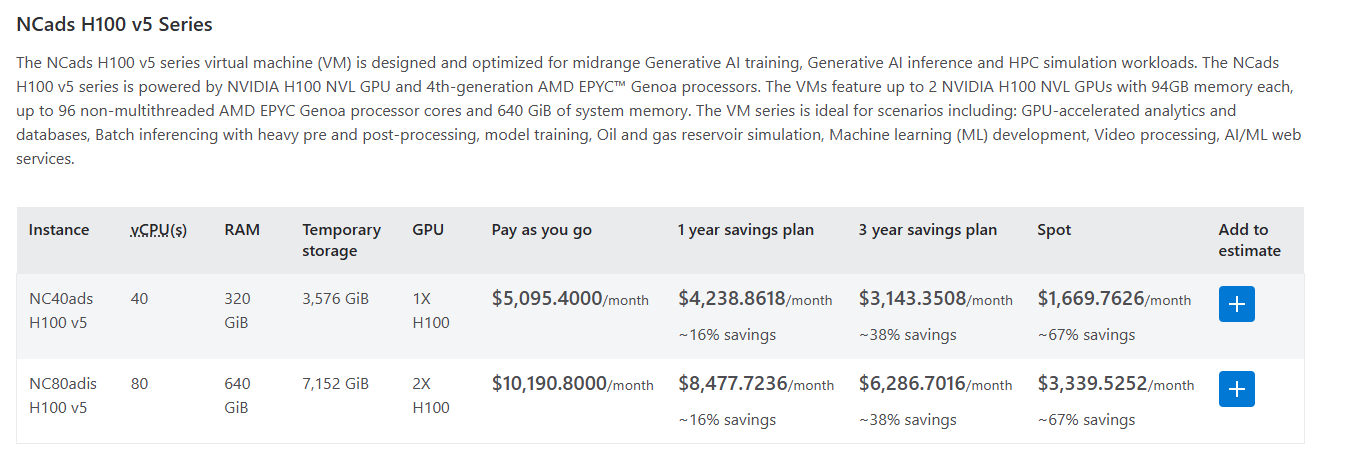

Check out the prices of data centre services below.

But wait. Those aren't good enough to run your AI-powered workflow.

Silly me.

Let's look at one with Nvidia's H100 chips.

Using the highest-powered models offered by AI providers, you can only run 1. with the configurations shown on the H100 chip comfortably.

Nevertheless, as taught in economics 101.

Increase demand, unchanged supply = higher price equilibrium.

For Oracle in the future, that is called - pricing power.

In a nutshell.

Don't get suckered by the news headlines.

Are AI stocks overvalued? Perhaps. Probably, even. But that's a separate question from whether the underlying adoption of AI is real, and whether Oracle's strategy is sound.

Valuation is a market sentiment problem. Oracle's capex spending is a strategic positioning decision.

The AI capex spending is not about earnings right now. It is about securing a seat at the table in the future.

So.

AI thematic remains in play.

As for the weakness in AI stock prices, if they begin trading at a more acceptable level, my view is that represents a buying/top-up opportunity for investors.